Market Insight from

Brulpadda and Luiperd have potential to spark an energy transformation in South Africa

South Africa has seen a flurry of activity in the past few years, which has led to two major offshore discoveries for the country: Brulpadda in February 2019 and Luiperd in October 2020. Potential development plans for the fields remain uncertain; however, it has been estimated that the two fields could hold resources of up to one billion barrels of oil equivalent each.

The significant resource potential has the ability to alleviate the country away from gas imports into the late 2020s, provide volumes sufficient to supply underutilised existing facilities, and perhaps even decarbonise South Africa’s currently heavily coal-fired power mix.

The South African gas market is very small on a global scale, with demand at approximately 500 million cubic feet per day (mmcfd) and just under 100mmcfd of domestic production. Most of the gas demand in the country is supplied by the Sasol owned Pande-Temane development in neighbouring Mozambique.

The gas to liquids plant in Mossel Bay has been running under capacity for the last few years as offshore domestic supply wanes. It is estimated that the plant ran out of feedstock gas at the end of 2020, forcing PetroSA to put out a tender for the supply of LNG to the plant in October of that year.

The South African demand for power is likely to continue growing as the economy develops and population grows. Currently, 87% of the South African grid is powered by coal. However, the government has stated its intentions to move away from coal-fired power, a move which could favour the newly discovered gas resources.

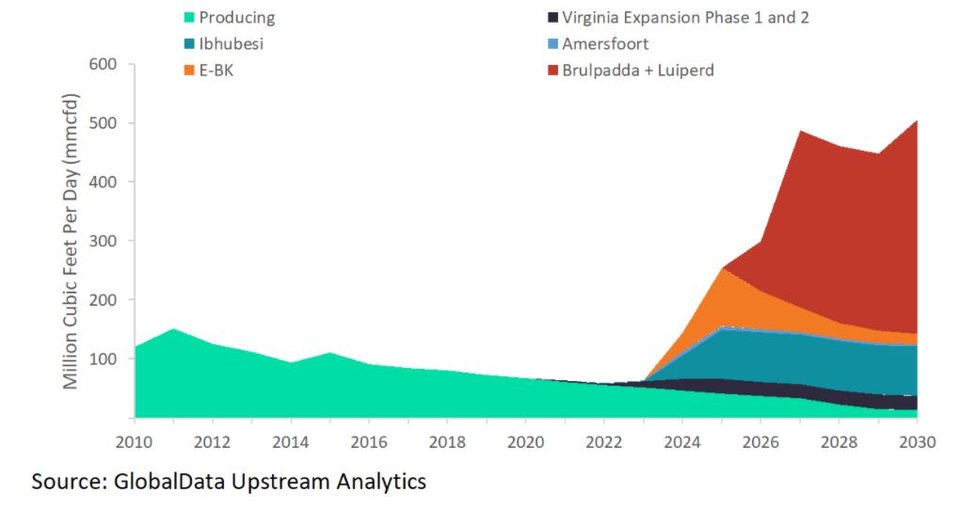

South Africa producing, planned, and announced gas fields, plus Brulpadda and Luiperd.

The potential development of Brulpadda and Luiperd is uncertain, but gas production could be sufficient to supply over half of the country’s current demand with first gas is unlikely before 2025. Along with the currently planned and announced projects, South Africa could become the majority supplier of its own gas demand for the first time in decades.

Production at existing fields is expected to decline over the coming decade, which will force the country to import more volume from Mozambique and seek alternative gas supply options such as LNG regasification to meet demand. In the current economic climate, a capital-intensive investment case will prove challenging and the partners will need to secure a clear gas commercialisation route that is favourable for both investors and the government.

South Africa is currently in the midst of updates to its fiscal framework that have been ongoing for a number of years and have led to multiple concerns. The current bill lacks legal certainty and stability, which has been one of the major obstacles for investment from international oil companies in the past.

Furthermore, other issues include how existing exploration rights (areas that do not have production) will be handled. In addition, details of royalties, production bonuses, and the new petroleum resource rent tax are lacking. Clarity on the changes is required to allow developments to be realised.

The country’s domestic gas supply is dwindling as their fields are in late life. With ambitions to decarbonise their economy and large investments into wind and solar panels over the last decade, more will need to be done in the medium term to move away from coal, which is where the new gas discoveries provide opportunity. However, development of the fields faces competition from proposed LNG and imports from Mozambique, leaving no clear route to monetisation at present.

For more insight and data, visit GlobalData's Oil & Gas Intelligence Centre.